Latest trend in the Islamic Fintech Industry

What is Islamic Fintech?

Islamic Fintech is a rapidly growing industry that combines the principles of Islamic finance with modern financial technology. It aims to provide financial products and services that are compliant with Shariah law, which prohibits interest-based transactions and promotes ethical and socially responsible investments.

Islamic Fintech meaning

Fintech is the merger of two terms: finance and technology. Islamic finance provides financial services to the customers in accordance to the rules and regulations prescribed by Shariah.

As Islamic finance is growing by leaps and bounds since the last two decades, and so is FinTech, in the last decade. The main objective of Islamic finance is to enhance the economic growth in the society with the use of Shariah compliant financial solutions.

Likewise, FinTech provides cost effective solutions for the companies and especially startups that help in the reduction of their costs and improvement in business processes. Financial industry is a very elusive yet important sector in the society, and hence heavily regulated by the regulators.

FinTech is a term flipped in the recent past for technological innovation in financial services. Regulators are working towards developing a standardised definition of this broad term. Currently there is no globally recognised definition for the term “FinTech.” (Schueffel, 2016) However, according to the Financial Stability Board (FSB), of the BIS 1, “FinTech is technologically enabled financial innovation that could result in new business models, applications, processes, or products With an associated material effect on financial markets and institutions and the provision of financial services” (Reserve Bank of India, 2017)

In recent years we have seen latest developments in the Islamic Fintech industry, such as the rise of crowdfunding platforms, the expansion of Islamic banking services, the increase in Islamic insurance offerings, and the growing interest from investors.

Understanding Shariah Compliance in Fintech

Shariah compliance is a crucial aspect of Islamic finance and fintech. It refers to the adherence to Islamic principles and laws in financial transactions and investments. In Islamic finance, Shariah compliance is mandatory, and any violation can result in severe consequences. Therefore, it is essential for Islamic fintech companies to ensure that their products and services comply with Shariah principles.

To achieve Shariah compliance, Islamic fintech companies must follow specific guidelines and regulations. These guidelines are based on the Quran and Sunnah and are interpreted by Shariah scholars. The scholars provide guidance on various aspects of Islamic finance, such as riba (interest), gharar (uncertainty), and maysir (gambling). They also evaluate the products and services offered by Islamic fintech companies to ensure they comply with Shariah principles.

Islamic fintech companies must also establish a Shariah supervisory board (SSB) to oversee their operations and ensure Shariah compliance. The SSB comprises Shariah scholars who are responsible for reviewing and approving the company’s products and services. They also monitor the company’s operations to ensure that they comply with Shariah principles.

Key Features of Islamic Fintech Products and Services

Islamic Fintech products and services have several key features that differentiate them from conventional financial products.

Firstly, they are designed to comply with Shariah law, which means they do not involve interest-based transactions or investments in industries that are considered haram (forbidden) such as alcohol, gambling, or pornography.

Secondly, Islamic Fintech products and services are often structured around profit and loss sharing models, where the investor and entrepreneur share the risks and rewards of a project.

Thirdly, they prioritize ethical and socially responsible investments, such as projects that promote sustainable development or support marginalized communities.

Fourthly, Islamic Fintech companies often use technology to increase access to financial services for underserved populations, such as those living in rural areas or without traditional banking relationships.

Finally, Islamic Fintech products and services are often more transparent and accountable than conventional financial products, as they are subject to independent Shariah audits and must adhere to strict ethical standards.

Examples of Islamic Fintech Companies and Offerings

Islamic Fintech companies are emerging all over the world, offering a range of products and services that cater to the needs of the Muslim community. Here are some examples of Islamic Fintech companies and their offerings:

- Wahed Invest: This is an online investment platform that offers halal investment opportunities to Muslims in the US and UK. The company uses a Shariah-compliant screening process to ensure that all investments are in line with Islamic principles.

- SalamWeb: This is a web browser that has been designed specifically for Muslims. It features built-in prayer times, Qibla direction, and a Halal food locator. The browser also blocks inappropriate content and promotes ethical online behavior.

- Ethis Ventures: This is a crowdfunding platform that focuses on ethical and socially responsible investments. The platform offers a range of Halal investment opportunities, including real estate, renewable energy, and healthcare projects.

- Zilzar: This is an e-commerce platform that connects Muslim buyers and sellers from around the world. The platform offers a range of Halal products, including food, fashion, and cosmetics.

- Amanah Advisors: This is a financial advisory firm that specializes in Shariah-compliant investments. The firm offers a range of services, including portfolio management, wealth planning, and Zakat calculation.

These are just a few examples of the many Islamic Fintech companies that are emerging around the world. Each company offers unique products and services that cater to the needs of the Muslim community, while also adhering to Islamic principles.

Crowdfunding platforms

Crowdfunding platforms have become an increasingly popular way for businesses to raise funds, while Islamic banking services have expanded to offer a variety of products and services in line with Islamic law. Islamic insurance offerings have also seen an increase in recent years, with companies offering products that are compliant with Islamic principles. All of these platforms are helping to drive the growth of Islamic Fintech and enable businesses and consumers to access financial services in line with their beliefs.

Halal Insurance

The Islamic Fintech industry has also seen an increase in Islamic insurance. Companies are offering products that are compliant with Islamic principles, such as halal insurance and takaful (mutual) insurance. These products provide an ethical way for businesses and consumers to protect themselves financially.

Murabaha Deposit

Murabaha Deposit is an Islamic short-term investment product based on the concept of Murabaha.

Murabaha Deposit allows you to make a healthy profit on your money in a safe and Shariah-Compliant manner. The Bank enters into a contract with you to invest your money in a selected commodity at an agreed price. You make a profit by selling the commodity at a future date at a higher price. (Read more on Murabaha)

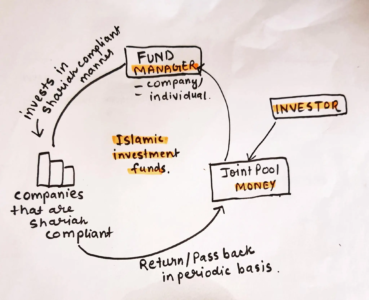

Islamic Investment Funds

The term “Islamic Investment Fund” means a joint pool wherein the investors contribute their surplus money for the purpose of its investment to earn halal profits in strict conformity with the precepts of Islamic Shari’ah.

Suppose there are investors who have with them surplus liquidity, but these investors do not have the skill and the ability to conduct business, so they would like to invest their surplus with somebody who is a skilled person who knows how to invest the money in strict conformity to shariah principles and give them a return

Islamic Fintech Malaysia

In Malaysia, Islamic finance has been a key driver of economic growth, with the country being one of the leading players in the global Islamic finance industry. The Malaysian government has been actively promoting Islamic finance as part of its efforts to position the country as a hub for Islamic finance and banking. With the emergence of fintech, the intersection of finance and technology has created new opportunities for the Islamic finance industry in Malaysia.

Fintech in Malaysia has seen significant growth in recent years, driven by factors such as increasing smartphone penetration, rising demand for digital payments, and a supportive government. According to a report by the Malaysia Digital Economy Corporation (MDEC), the country’s fintech industry is expected to reach a value of RM 21 billion (USD 5 billion) by 2024.

The fintech landscape in Malaysia is diverse, with startups operating across various segments such as payments, lending, wealth management, and insurance. Some of the notable players in the industry include GrabPay, Boost, Funding Societies, and PolicyStreet. These companies have leveraged technology to offer innovative solutions that cater to the evolving needs of consumers.

The Malaysian government has also been proactive in promoting fintech innovation, with initiatives such as the Malaysia Tech Entrepreneur Programme (MTEP) and the Fintech Booster programme. The central bank, Bank Negara Malaysia, has introduced regulatory sandboxes to enable fintech startups to test their products and services in a controlled environment.

Overall, the fintech industry in Malaysia is poised for continued growth, with ample opportunities for startups to disrupt traditional financial services. The emergence of Islamic fintech, in particular, presents a unique opportunity to tap into the country’s large Muslim population and provide Shariah-compliant financial solutions.

Islamic fintech companies in Malaysia have also been successful in attracting funding from investors. In 2019, Malaysian Islamic fintech companies raised over $100 million in funding, indicating the potential for growth in this sector.

In Malaysia, there are several key players in the Islamic Fintech industry that are making significant contributions to the growth and development of this sector. One of the leading companies is Ethis Ventures, which provides an online platform for peer-to-peer (P2P) crowdfunding that adheres to Shariah principles. The company has successfully raised funds for various projects, including affordable housing and renewable energy initiatives.

Another prominent player is HelloGold, a mobile app that allows users to buy and sell gold using blockchain technology. The app is fully compliant with Shariah law and offers a secure and convenient way for Muslims to invest in gold without having to worry about storage or safety issues.

Meanwhile, Wahed Invest is a robo-advisor platform that offers Halal investment portfolios to its clients. The company uses a combination of human expertise and artificial intelligence to create diversified portfolios that are in line with Islamic principles.

Other notable players in the Islamic Fintech industry in Malaysia include EthisKapital, a P2P lending platform that focuses on ethical financing, and SkolaFund, a crowdfunding platform that helps students finance their education.

These companies are just a few examples of the innovative and forward-thinking businesses that are driving the growth of Islamic Fintech in Malaysia. By offering Shariah-compliant financial products and services that cater to the unique needs of Muslim consumers, they are helping to create a more inclusive and sustainable financial system for all.

Bursa Suq Al Sila: Being the financial hub for Islamic Fintech Malaysia.

Islamic Finance, Malaysia made its position much stronger by initiation of trade on the world’s first completely Shariah compliant, electronic commodity trading platform, called Bursa Suq Al Sila. It is a global commodity platform for facilitating asset-based Islamic financing and investment transactions under the Shariah guiding principles of Murabahah, Tawarruq and Musawwamah. The underlying commodity in Bursa Suq Al Sila is crude palm oil (CPO). It is an initiative by the Malaysia International Islamic Finance Center (MIFC). The trading platform is operated by Bursa Malaysia via its fully Shariah-compliant wholly owned subsidiary, Bursa Malaysia Islamic Services Sdn. Bhd (Islamic Finance News, 2013).

Role of Shariah Scholars in Islamic Fintech Industry

The Fintech ecosystem includes, fin-tech startups, technology developers, governments, financial customer, traditional financial institutions, regulators, and in the case of Islamic Fintech role of shariah board/shariah scholars is also very important.

Fintech for Islamic Finance must observe Shariah guidelines. In general, technology is neutral from Shariah perspective, unless it is used in a instance directly conflicts with any rulings or requirements of the Shariah (Oseni & Ali, 2019). But, how do we determine which FinTech apphcation that requires sensitivity to Shariah requirements? Prof. Akram Laldin, Executive Director ISRA answers this in the following words.

“In order to address these concerns, it is important to note that, in general, Shariah principle with regards to a business transactions (Muamalat) is governed by the notion that every transaction is permissible, except when there is a clear text which prohibits it. The permissible principle provides flexibility in innovation and new practices in business and financial transactions.

All innovations in Muamalat, are considered as permissible and welcomed. In this regard, innovations in FinTech become impermissible only if there is clear evidence that they are in conflict (against) the basic rules of the Shariah. Therefore, FinTech application and practices, as in traditional Islamic finance, should follow the principles of the Shariah by avoiding the prohibited elements in the transactions such as interest (Riba), gambling (Maysir), uncertainty (Gharar), harms (Darar), cheating (Tadlis), etc. It must be transparent with no hidden cost, irresponsible or unethical financing’ .

This gives us the fundamental guideline of what ‘Shariah compliance’ means in Fintech. The use of FinTech in a particular Islamic finance product should not be such as to create harm, deception/ cheating, hidden costs, nor should it inculcate any Riba, gambling, Gharar, or other prohibited elements such as those that make the sale invalid.

He continued: “Likewise, the practice of transactions in FinTech application should follow the rules of contract (Aqd) used in the transaction by observmg the pillars (Rukn) and conditions (Shan) in the contract. In addition, FinTech application should aim at achieving the objectives of the Shariah (Maqäsid Al Shariah), namely, to realize the benefits (Maslahah) and to avoid the harms and difficulties (Mafsadah and Mashaqqah)”

Even though FinTech was not especially well-known within the Islamic Finance industry until late 2015,

the progress of 2016 and 2017 demonstrate some wonderful accomplishments.

You can read more here.

Hope you enjoyed reading this article on Islamic Fintech Industry. If you are interested on reading more on Islamic Finance, do let us know in the comment box below.

Discover more from Islam Hashtag

Subscribe to get the latest posts sent to your email.