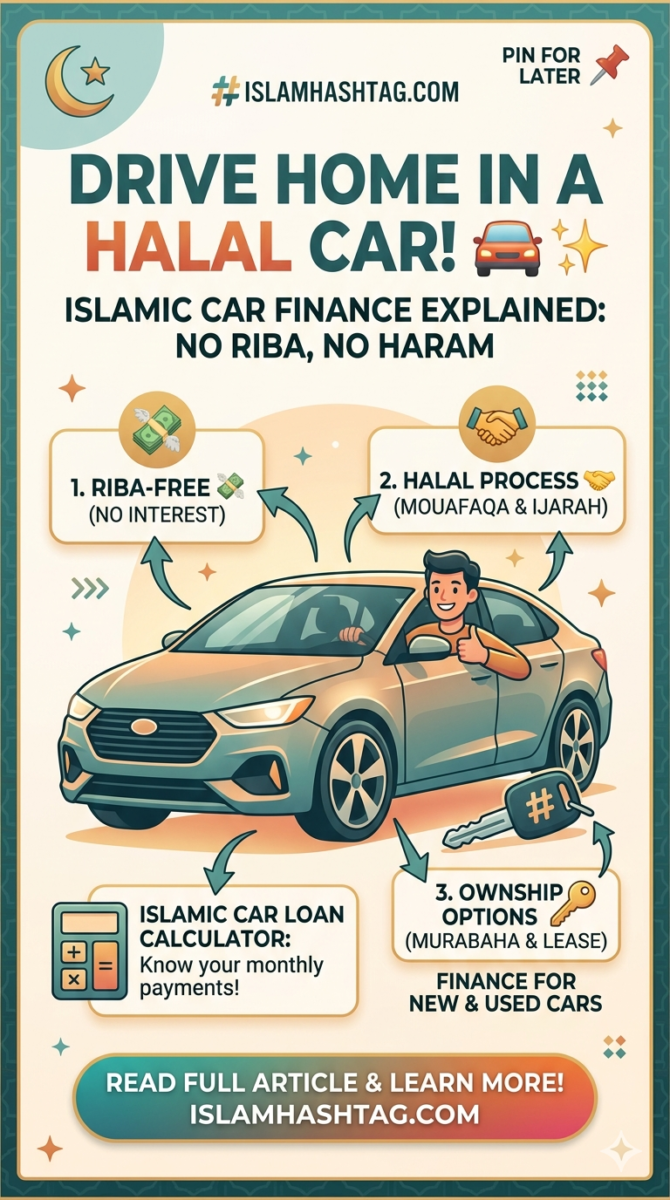

Halal Car financing : About Islamic car finance and halal Car Loan

In 2023, Islamic car finance continues to gain prominence as a preferred option for Muslim drivers in the USA, Canada, UK, and Australia who want to adhere to the principles of Sharia law while acquiring a vehicle. This financial solution, known as halal car finance, ensures that the entire process aligns with Islamic ethical guidelines, making it a viable and Sharia-compliant alternative to conventional auto loans. In this article, we’ll explore the intricacies of halal car finance and the key components that make it compliant with Islamic principles.

What Is Halal Car Finance?

Halal car finance, also referred to as Islamic car financing or Islamic car loans, is a financial facility provided by Islamic lenders to assist Muslim drivers in financing their vehicle acquisitions while adhering to Sharia law. Unlike conventional auto loans, which involve the payment of interest (Riba) – a practice forbidden in Islam – halal car finance operates on principles that align with Islamic ethics.

What Constitutes an Islamic or Halal Car Insurance?

For a vehicle to be considered truly Islamic or halal, it must meet specific criteria that align with Islamic principles:

- Ethical Manufacturing Conditions:The vehicle’s manufacture must adhere to ethical standards, avoiding materials such as leather from pork and prohibiting child labor in the production process.

- Sharia-Compliant Financing: The vehicle’s financing must be in accordance with Islamic Sharia, often following the Murabaha principle.

- Halal Auto Insurance (Takaful):The vehicle and its occupants should be covered by insurance that operates within the framework of Islamic finance.

Meeting these conditions ensures that the vehicle aligns with Islamic principles and can be considered halal.

The Appeal of Islamic Car Finance

Islamic car finance has become a favored choice for strict Muslims for several compelling reasons:

- Sharia Compliance: It aligns with Islamic principles by eliminating interest-based transactions, ensuring that every aspect of the financing process adheres to Sharia law.

- Monthly Payments: Islamic car finance allows individuals to spread the cost of a car over time through manageable monthly payments, making vehicle ownership more accessible.

- Ethical Financing: It offers an ethical and responsible alternative to conventional financing options, which often involve interest, considered unethical in Islam.

The Nuances of Halal Car Finance

While Islamic car finance offers numerous advantages, it’s important to recognize that it’s not just an easy way to secure an interest-free car finance deal. Here are some key aspects to consider:

The Borrowed Amount:

- The amount borrowed in Islamic car finance typically equals the price of the car plus any profit (akin to interest) that a seller might charge. This profit is earned through the principles of Murabaha, Ijarah, or Musharakah, which align with Islamic finance guidelines.

Pros of Islamic Car Finance:

- Sharia Compliance: It adheres to Islamic financial principles, ensuring that transactions are ethical and Sharia-compliant.

- Accessible Vehicle Ownership: It makes owning a car more accessible by allowing individuals to pay for it over time rather than requiring a lump-sum payment.

- Mutually Beneficial: Islamic car finance often fosters a mutually beneficial relationship between the buyer and the financing provider.

Cons of Islamic Car Finance:

- Higher Initial Cost: The cost of the car under Islamic finance may be slightly higher due to the inclusion of profit for the financing provider.

- Complexity: The structuring of Islamic car finance can be more intricate than conventional financing, requiring a deeper understanding of Islamic finance principles.

- Limited Availability: Depending on the region, Islamic car finance options may be limited compared to conventional financing.

How Does Halal Car Finance Work in 2023?

Common Structures of Islamic Car Finance:

- Murabaha: This is a cost-plus financing arrangement. The Islamic finance provider purchases the vehicle and then sells it to the customer at a marked-up price, allowing the customer to pay for the vehicle over time. This structure provides transparency in pricing.

- Ijarah: Under this leasing agreement, the finance provider purchases the vehicle and leases it to the customer for an agreed-upon rental fee. At the end of the lease period, the customer may have the option to purchase the vehicle.

- Musharakah: This is a shared ownership financing model. Both the customer and the finance provider jointly own the vehicle, and the customer gradually buys out the finance provider’s share, ultimately becoming the sole owner.

Murabaha Car finance

The fundamental structure of a halal car loan in 2023 is based on the principle of Murabaha, a commonly used mechanism by Islamic banks to facilitate vehicle purchases for Muslim drivers. Here’s how it works:

- Vehicle Selection: The driver selects the desired vehicle they wish to purchase.

- Financing Request: The driver submits a financing request to the Islamic bank.

- Purchase by the Bank: The Islamic bank purchases the chosen vehicle in its name.

- Vehicle Handover: The bank then transfers possession of the vehicle to the driver.

- Monthly Installments: The driver enters into an agreement with the bank to pay monthly installments for a pre-agreed period, which includes a profit margin for the Islamic lender.

- Ownership Transfer: Once all monthly payments are completed, ownership of the car is transferred to the driver.

This process ensures that the acquisition of the vehicle is done in a manner that complies with Islamic financial principles, without the involvement of interest-based transactions.

when using Halal car finance, the dealer pre-loads the interest cost onto the price of the car, making it a fixed and transparent amount for the buyer. This way, the transaction complies with Islamic principles.

Islamic Investment Funds and types of Islamic shariah investment

Halal Car financing example (Murabaha):

For Example-

- Traditional Financing (Non-Halal):

- Price of the car: £10,000

- APR: 5%

- Contract length: 12 months

- Total cost to buy the car (including interest): £10,500 (£10,000 for the car + £500 in interest)

- Halal Car Finance (Murabaha):

- Price of the car: £10,500 (interest pre-loaded onto the price)

- APR: 0%

- Contract length: 12 months

- Total cost to buy the car: £10,500 (same as the initial price)

In the Halal car finance option, there is no additional interest charged, and the total cost to buy the car remains £10,500, which is fixed and known upfront. This adheres to Islamic finance principles because it avoids interest-based transactions.

Please note that the specific terms and structures of Halal financing may vary depending on the institution offering the finance and the jurisdiction in which it operates. Islamic finance seeks to ensure that financial transactions are ethical and compliant with Islamic law.

Eligibility and Requirements:

Eligibility criteria for Islamic car finance typically include:

- Proof of income and employment

- A good credit history

- Compliance with Islamic principles

- Documentation to establish identity and financial standing

Islamic Takaful Auto Insurance

An integral part of the halal car ownership experience is Islamic Takaful auto insurance. This form of insurance covers a halal car against various risks while adhering to the principles of Islamic finance. It’s crucial for ensuring that both the vehicle and its occupants are protected through lawful means, aligning with the ethical requirements of Islamic law.

Takaful and Car Insurance

When individuals opt for Islamic car financing through entities like Islamic banks or financing firms, it is common practice for the financier to recommend Takaful as the preferred car insurance option. In the context of motor Takaful, participants contribute to a general Takaful fund by offering a sum of money as a participatory contribution known as “tabarru’.”

Through an agreement (aqad), participants become part of a mutual assistance pact, committing to assist one another in the event of a loss arising from an accident involving any of the participants’ cars. In essence, motor Takaful serves as a Sharia-compliant alternative to conventional car insurance, addressing the need for asset protection while adhering to Islamic ethical principles.

Islamic Car Financing USA

As the demand for Sharia-compliant financial solutions continues to rise, halal car finance emerges as a key player in providing Muslims in the USA, Canada, UK, and Australia with a way to own vehicles while remaining true to their faith.

Al Rayan and Lloyds TSB provide Islamic bank accounts.Some other banks- like Amana Mutual Funds Trust and Manzil USA can also offer Islamic Car finance. They may also help in Islamic truck financing, Islamic auto financing and Islamic car financing. But It is important to contact them and inquire if they offer Islamic Car loan.

Top 5 Financial Companies Providing Shariah Loans in Australia

Reference-

- https://www.parkers.co.uk/car-leasing/advice/islamic-car-finance-explained/

Follow us in Facebook for more updates or Subscribe

Discover more from Islam Hashtag

Subscribe to get the latest posts sent to your email.